By Usman Aliyu, News Agency of Nigeria (NAN)

By 6 a.m., the Post Office motor park in Ilorin was already awake.

Commercial buses revved impatiently as conductors shouted destinations to Osogbo, Iwo and Ibadan, while hawkers threaded through commuters balancing baskets of bread, soft drinks and sachet water.

A few metres away, Halimat Opakunle arranged neat bundles of naira notes, switched on her Point-of-Sale (POS) terminal and prepared for what she expected would be another ordinary business day.

For nearly five years, the mother of five had followed the same routine. Unable to secure formal employment after graduation, Opakunle turned to agent banking, joining thousands of Nigerians who have built livelihoods by bringing financial services closer to communities where banks are scarce and ATMs frequently fail or are unavailable.

“There was no job after I graduated. That was why I started the POS business,” she recalled.

However, nothing about June 2, 2025, suggested her life was about to change. Two young men approached her, saying they were travelling to Iwo in Osun, ahead of the Eid-el-Kabir celebration.

One withdrew N100,000, paying a N2,000 service charge. Moments later, they requested a transfer of N700,000, explaining that someone in Iwo needed to buy rams before prices rose.

One of the men produced a debit card, inserted it into the POS terminal himself and entered the correct Personal Identification Number (PIN). The terminal displayed a familiar message: APPROVED.

Opakunle transferred the money to the account they provided. The customers thanked her and disappeared into the morning crowd.

Nearly two weeks later, she received a police invitation. Investigators told her the debit card used in the transaction had allegedly been stolen.

“I didn’t know it was a stolen card. They brought the ATM card themselves. They inserted it themselves and entered the PIN. How was I supposed to know it was a stolen card,” she said.

That single transaction has since drawn Opakunle into a prolonged legal battle. Court appearances now compete with business hours, reducing her income and draining family savings.

Her father even paid N25,000 to obtain National Identification Number (NIN) records that investigators believed could help trace the recipient account.

When a suspect was reportedly identified in Abuja, the family offered to fund the logistics for his arrest, but the case instead proceeded to court.

“I’ve just continued going to court. There is nothing else I can do,” she said quietly.

The Unseen Risk of Financial Inclusion

Halima’s experience is not an isolated case. Her ordeal reflects a little-known consequence of Nigeria’s digital payments revolution.

While the rapid expansion of digital banking has driven unprecedented financial inclusion, interviews with the POS operators across the city, officials of the Kwara Association of Professional Point-of-Sale Agents (KAPPSA), law enforcement authorities, and fintech experts reveal a troubling tension at the heart of Nigeria’s cashless revolution.

The same neighbourhood entrepreneurs driving financial inclusion are increasingly finding themselves under criminal investigation after fraudsters allegedly exploit gaps in the country’s digital payment system.

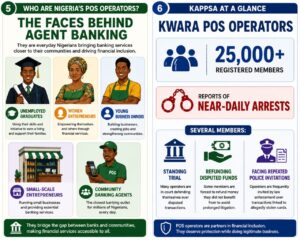

Over the past decade, POS operators have become the face of banking for millions of Nigerians, processing withdrawals, transfers, bill payments and deposits while creating livelihoods for thousands of unemployed graduates, women and young entrepreneurs.

In communities where bank branches are scarce, ATMs frequently run out of cash and internet banking remains unreliable, they have become the closest thing to a neighbourhood bank.

According to the Central Bank of Nigeria (CBN), more than 2.93 million POS terminals had been deployed across the country by the first half of 2024, up from 2.45 million six months earlier. During the same period, POS terminals processed 6.4 billion transactions valued at N85.9 trillion, reflecting Nigerians’ growing reliance on neighbourhood agents for everyday financial services.

Yet for many operators, every transaction now carries an unseen risk.

Abubakar Ibrahim knows that feeling well too. After struggling to secure formal employment, the graduate built a thriving POS business, expanding from one outlet to three in Ilorin. Then one customer arrived carrying two debit cards. The first transaction failed. The second went through.

Months later, investigators informed him that the cards had allegedly been stolen. Determined to avoid prolonged litigation, Ibrahim eventually paid more than N200,000 to settle the matter – money he insists he never benefited from.

“If I had used that money to feed my family, I would know they benefited from it. Instead, it felt like I threw my hard-earned money into fire,” he said.

Gbenga Adaramola, a zonal chairman of KAPPSA, recalled rushing to the Nigeria Security and Civil Defence Corps (NSCDC) headquarters after one of his members was arrested over a N300,000 withdrawal allegedly made with a stolen card.

Ironically, the operator had borrowed cash from neighbouring POS agents to complete the transaction because he lacked sufficient liquidity.

“The commission he made was about N2,500. He didn’t even have the money. He sourced it from other operators just to satisfy the customer,” Adaramola said.

After more than a year in court, the case was dismissed when inconsistencies emerged in the prosecution’s evidence.

For Oyewole Ariyo, the ordeal began when his business account was frozen months after a customer allegedly withdrew N158,000 using a stolen debit card.

Fortunately, Ariyo had kept handwritten records of large transactions. When investigators showed him photographs of suspects, he immediately recognised the customer.

Although investigators later identified the suspect, Ariyo said his account remained frozen for more than two months, disrupting his business.

The Legal Burden on Operators

Individually, each case appears unrelated. But together, they reveal a recurring pattern; a customer presents a physical debit card, enters the correct PIN, the banking system approves the transaction, and days or weeks later investigators arrive after the card is reported stolen.

To Ridwan Opakunle, Chairman of KAPPSA, the pattern exposes a gap in Nigeria’s rapidly evolving digital payments ecosystem.

“Our members are not against investigations. If someone commits a crime, the law should take its course. But operators who merely provide legitimate banking services should not bear the burden of proving their innocence simply because a transaction passed through their terminals,” he said.

Most operators, he said, were young entrepreneurs or women running small businesses with limited capital.

“When an account is frozen or an operator is repeatedly attending court, it is not just the business that suffers, it affects families, children’s school fees and the livelihoods of people who depend on that income,” he said.

Opakunle said KAPPSA’s more than 25,000 registered members have been affected by near-daily arrests, with several operators standing trial or refunding disputed sums over transactions linked to allegedly stolen debit cards.

He called for stronger collaboration among regulators, banks, fintech companies and security agencies to protect both victims of fraud and innocent operators.

“We all want fraudsters arrested. But we also need a system that identifies the real criminals without discouraging the people helping to expand financial inclusion across Nigeria,” he said.

Meanwhile, while the affected POS operators alleged repeated arrests, extortion and unfair treatment by some security operatives, law enforcement authorities rejected claims that POS agents are automatically treated as suspects in cases involving stolen debit card transactions.

According to ASC Shola Ayoola, Public Relations Officer of the NSCDC in the state, investigations are driven by evidence, not assumptions.

Ayoola explained that unlike ATMs, which operate without direct human interaction, POS terminals are managed by identifiable individuals who may have physically encountered the customer.

“That makes the operator a vital point of inquiry,” said the NSCDC spokesperson.

He stressed that investigators first analyse transaction records, interview relevant persons and review available evidence before deciding whether an arrest is necessary.

The spokesperson of the police in Kwara, SP Adetoun Ejire-Adeyemi shared the same position.

According to her, POS operators are usually questioned because they represent the last known physical point where the disputed transaction occurred.

“The objective is to establish facts, not assumptions,” she said, explaining that investigators rely on transaction records, witness statements, CCTV footage where available and other digital evidence before making arrests.

Both agencies acknowledged that investigations sometimes cleared people initially suspected and supported stronger technology to improve evidence gathering.

They also admitted that tracking financial fraud has become more difficult as criminals constantly change tactics, using stolen identities, multiple bank accounts, improperly registered SIM cards and rapidly moving funds across several accounts before victims discover the theft.

The absence of surveillance technology at many POS locations, they maintained, further complicates investigations.

That is where fintech experts believe Nigeria’s digital payments ecosystem must evolve.

Layered Biometrics as a Path Forward

Mr Hussein Olarewaju, founder, HAQ Technology Management Services, said financial institutions already deploy sophisticated fraud detection systems capable of monitoring unusual transaction patterns, unfamiliar devices and suspicious account activity.

He noted that the CBN had introduced liveness testing for certain high-risk transactions, enabling financial institutions to compare a customer’s live facial image with existing Know Your Customer (KYC) records before approving payments.

Although implementation is still evolving, he believes similar safeguards should be extended to agent banking.

“Smart POS terminals can integrate BVN, NIN and liveness testing to verify customer identity,” he said.

Similarly, fintech and compliance expert Olakunle Afolabi agreed that the current card-and-PIN system is no longer sufficient.

According to him, fraudsters increasingly obtain both debit cards and PINs through theft, deception or social engineering.

His solution is layered biometric authentication.

“Fingerprint or facial verification should complement PIN authentication, especially for high-value transactions. That additional layer will significantly reduce fraud at agent locations,” he said.

Both experts also see value in camera-enabled smart POS terminals, though Afolabi cautioned that photographs should complement – not replace – biometric verification.

While the experts acknowledged that deploying such technology would increase operational costs, they argue, however, that the cost of stronger identity verification is far lower than the economic losses caused by fraud investigations, frozen business accounts and prolonged court cases involving innocent operators.

Interestingly, their recommendations mirror those of both the Police and the NSCDC, which believe enhanced identity verification would help investigators identify actual offenders while reducing the likelihood of innocent operators becoming entangled in investigations.

This convergence suggests that while operators and investigators may disagree over individual cases, they increasingly agree on the solution.

For KAPPSA Chairman, that solution must also include clearer operational guidelines that recognise the realities facing neighbourhood agents.

He urged regulators, payment service providers and security agencies to work together on practical reforms, including improved KYC procedures for high-value transactions, continuous training for agents, faster information-sharing between banks and investigators, and stronger safeguards against unnecessary disruption of legitimate businesses.

“Our members are partners in financial inclusion. They are helping government and financial institutions take banking to communities where there are no bank branches. They deserve protection too,” he said.

As dusk settles over the motor park, Halimat Opakunle packs the remaining cash and prepares to close. Tomorrow, she will return before sunrise, serve another queue of customers and wait for the familiar message on her POS terminal: APPROVED.

For millions of Nigerians, it simply confirms a successful transaction. For Opakunle, it now carries an unsettling question; could another routine transaction end with a police invitation or a courtroom appearance?

As Nigeria deepens its cashless economy, the challenge is no longer just expanding digital payments.

It is building a system where technology, regulation and investigations can identify fraudsters without casting innocent neighbourhood entrepreneurs, the very people driving financial inclusion, as unintended suspects. (NAN)